Forget About the Price Tag, Jessie J.

Reporter's Notebook: March 24, 2022

Welcome to Please Haul My Freight: Edition 18. Here are some items in my notebook this week:

XPO LATEST: No news on XPO’s plans to sell domestic intermodal (the old Pacer business) and/or drayage. Multiple suitors looked under the hood and didn’t like what they saw, or thought the asking price was too high, according to my sources.

Meanwhile, XPO has released an investor Q&A. Here are some highlights, but remember to take corporate spin with a grain of salt.

NORFOLK SOUTHERN1: An overhead crane caught fire late Monday in Norfolk Southern’s Jacksonville terminal, just weeks after resolving another problem in NS Jacksonville. There have been more than a dozen disruptions in NS Jacksonville since January 2021.

Here is what NS said on the fire:

“From initial reports, operationally, damage was limited to the single crane. The rail car below it, as well as three loads, were inspected. Members of Norfolk Southern’s terminal operations team have reviewed the overall impact and adjusted inbound/outbound loadings to/from our Jacksonville facility accordingly.”

One non-asset IMC told me:

“The problem is they are [often] on the verge of something happening to put them back in the ditch. It’s been like this for the past 12 months in Jacksonville. They clean up enough to operate, and then one hiccup brings it all down.”

Here is what NS is doing long-term to address disruptions:

Starting in 2018 and comes online later this year.

Started design our current expansion “Kowkabany” expansion

130 added parking spots, an improved ingate/outgate, and a new crane

Estimated at 35,000 added annual lifts, or 13%

Expanded our Titusville offering to divert Central Florida destined volumes out of JAX to Titusville: Diverted 16K loads in 2021.

We added 3 satellite ramps in 2021, between March and May. We went from 1,200 to 1,500 parking spots with these satellite ramps, an increase of 25%

We have 5 overhead cranes and 1 side loader today. We added the side loader in late December 2021.

J.B. HUNT: Last week, J.B. Hunt and BNSF Railway announced an expanded intermodal partnership that is a response to Schneider National leaving for Union Pacific. I asked a trusted source on intermodal for his thoughts:

“This would give Hunt the capabilities to handle about 3.25 million loads. The industry can’t grow that fast, so their share of domestic intermodal will rise from about 33% today to over 50%.”

150,000 containers X 1.8 box turns per month X 12 months= 3.24 million.

The math assumes shippers and receivers get back to normal equipment turns. But if J.B. Hunt owned 150,000 containers, then a 50% market share is not out of reach.

It also depends on how much Hub Group and Schneider grow in the next five years.

BNSF’S FUTURE: I had a lengthy exchange with BNSF on how they are supporting their customers in 2022. Here is part of what BNSF told me:

Crews have begun working on a significant capacity project at our Cicero Intermodal Facility to create 400 additional parking stalls. This expansion is part of a multi-year project that includes additional production track and parking capacity to support intermodal growth. We are confident that these additions will deliver greater service and productivity at our Chicago intermodal facilities.

In North Texas, we will complete a multi-year expansion of our Alliance Intermodal Facility. Most notably, the expansion will provide approximately 1,100 parking stalls.

We are currently engaged in a multi-year effort to add several segments of new double-track in eastern Kansas. Between Emporia and Wellington, we expect to have approximately 35 more miles of second mainline track placed into service by the end of the year. Once completes, approximately 50 miles of new double-track will be available to support traffic growth.

Additionally, we plan to add approximately 1,250 well cars into service this year that can carry approximately 2,500 containers.

THE IMPACT OF FUEL: How will fuel prices play out for the rest of the year? And how will that impact truckload rates? I don’t know. Here is JOC’s Shipper Truckload Spot Rate Index, based on outbound rate data from Cargo Chief, DAT Solutions, and digital broker Loadsmart2:

(greater than 250 miles)

Remember dry-van rates are supposed to fall in February and March. Given this data, I suspect our JOC Domestic Intermodal Savings Index, spot and contract, will drop for a second consecutive month in March. The Index base is 100.

TRUCKING OUTLOOK: Are we seeing a typical market slowdown in truckload, or are there long-term implications? Justin Stone, a supply chain manager for Pepsi Logistics, gave his thoughts on LinkedIn:

“Despite Morgan Stanley's March Freight Transportation report projecting H2 of 2022 to match that of 2021, I believe we'll see H2 2022's load-to-truck ratios be more in line with 2017/2020, an increase in inventory levels and a projected decrease in consumer spending, indicators of demand slowing.

Truckload capacity becomes more readily available with buying patterns shifting more toward pre-COVID 19 levels by H2 of 2022. I do not expect truckload rate-per-mile to reflect the peaks we saw in H2 2021. However, I do anticipate contractual rates remaining inflated (2018 level) due to an increase in costs of goods (tractors, trailers, diesel), labor (drivers), and services (insurance).”

CHARLESTON: The South Carolina Ports Authority has now stopped giving out a timeline on when it will clear the 25 vessels anchored outside Charleston. The average vessel wait time is ~10 days. Here is what CEO Jim Newsome told me:

“We have never experienced this before. It was a new thing for us starting at Thanksgiving. We probably underestimated the impact of some of the earlier diversions from [Savannah] that came here. I think there are just too many moving parts to this. I mean, we only control so much of what happens in our port.

Our main focus will continue to be on getting the import volumes down because I think that's the key to getting out of this. But as we've worked hard to get import dwell down, we get more empty containers back, while exports are still coming to go on ships. We’ve improved on the metric that we really were focused on, but the other two metrics have crept up.

The only thing that we can do is put [exports and empties] onto ships because there's nowhere else for them to go.

But if you looked at our February numbers, we are 2 to 1 imports versus exports, and that's the most imbalanced we've ever been, so that means you got to put record numbers of empties back on ships.”

The port also received an appropriation from the state legislature to fund on-dock rail in the Leatherman Terminal in 2025.

PORT STRIKES: In our notebook “The TPM 2022 Edition” we mentioned how shippers are planning for a West Coast port strike. Paul Berger (a GOOD REPORTER) has an article about this topic. Charleston is not an option right now, and getting a booking to another major US East Coast port is pretty difficult too.

Ports such as Baltimore or Jacksonville have open berths right now, but there are other challenges with using a smaller port.

IPI VOLUME: The number of ocean containers leaving the West Coast on trains rose month over month in February, according to the Intermodal Association of North America. This is the first time February IPI volume was higher than January since we began collecting IANA data in 2013. It also explains why the spot truckload rates in the Southwest and Northwest have fallen in the last 60 days (see screenshot above):

So what’s the situation with marine chassis?

From a Chicago dray source:

“Zero pool inventory (DCLI, Flexi, and TRAC). We cannot depend on the equipment providers. Union Pacific Global IV is the only facility mounting all containers. BNSF LPC has slowly started stacking more than 75%.”

From a Midwest dray source:

Columbus OH: Chassis shortage has gotten worse from exports sitting awaiting in gates. Imports are slow to unload at customers as well.

Cincinnati, Cleveland (OH), Detroit, Louisville: Hit or Miss; Depends on the week or any given day. IEP’s releasing small amounts of chassis here and there.

From a Kansas City dray source — UP’s no cherry picking policy is a problem again:

The chassis situation is dire here for 40-foot chassis, specifically TRAC for CMA CGM. This poses an issue as there are so few TRAC chassis available, yet many CMA boxes. UP will stack the boxes until they get TRAC chassis in, and won’t unstack the boxes for us, even if we have a private chassis. They continue to charge the rail storage fees, but won’t let you get the box out. Our chassis issues are not nearly as bad today as they were months ago for most of the ocean carriers — CMA CGM is the main issue right now.”

From a Memphis dray source:

“The rails are not congested anymore except for certain times of the day, but it is still taking BNSF several hours to turn a driver. Chassis have not been an issue until recently and it’s a very slight issue.”

From a Dallas-Ft. Worth dray source:

“UP has seen a little interruption. BNSF Alliance experienced some unique challenges which created a container stacking situation, but we are seeing more units being mounted.”

My NVO sources expect more growth in March because ocean carriers are interested in spot IPI opportunities, but not necessarily IPI under an annual contract.

OSRA LEGISLATION: The Senate Committee on Commerce, Science, and Transportation unanimously passed the Ocean Shipping Reform Act out of committee this week. The U.S. Senate now takes up the bill, and then a conference committee would iron the differences between S. 3580 and H.R. 4996 (the House version).

DEMURRAGE CASE: The FMC issued an updated final ruling on Tereno v. C.H. Robinson this week, after an initial ruling in January. Tereno (importer) alleged C.H. Robinson (NVOCC) assessed demurrage in violation of the U.S. Shipping Act. The administrative law judge ruled the customs broker Clearit — not C.H. Robinson — acted too slowly to clear the hold. The FMC clarified passing on an ocean carrier penalty is not a defense in and of itself, but Tereno couldn’t prove C.H. Robinson acted unreasonably here.

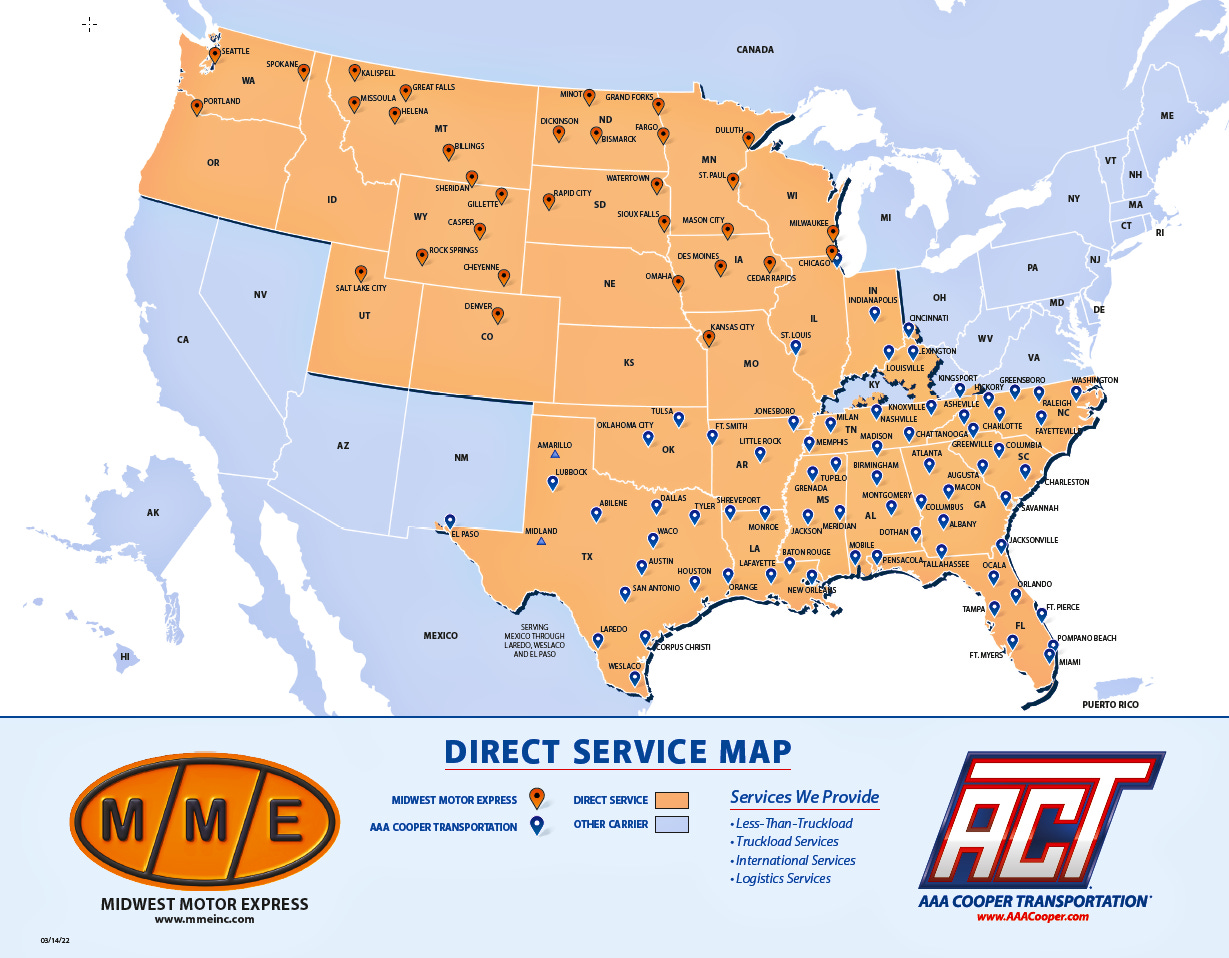

LTL INTRIGUE: A. Duie Pyle is opening new terminals in Richmond, Roanoke, and Manassas, Virginia. Meanwhile, Knight-Swift Transportation wants to construct a national LTL network. Knight-Swift purchased AAA Cooper Transportation and Midwest Motor Express in 2021, but there are two holes still left to fill.

Guess which LTL fills one hole? A. Duie Pyle. (see maps)

Who would KNX buy on the West Coast? Oak Harbor Freight Lines. Maybe Dependable Companies, if not Oak Harbor.

TEAMSTERS: Sean O’Brien replaced Jimmy P. Hoffa in the top post at the International Brotherhood of Teamsters. From Amit Mehotra of Deutsche Bank:

The contract negotiations with UPS are in 16 months and demands include $20/hour minimum pay for part-time workers and removal of in-truck cameras. Ultimately, O’Brien plans to negotiate a contract with UPS, which can be used as a model to convince others such as Amazon employees to unionize…

We believe the upcoming contract negotiation between UPS and the Teamsters has potential to be the most tumultuous since the 15-day UPS work stoppage in 1997.

CHASSIS: The IEPs are forging direct relationships with chassis manufacturers. TRAC Intermodal announced a partnership last week. From the press release:

LB Steel is building frames for new chassis and Integrated Industries is blasting, painting and installing all equipment components at its Dixmoor, Illinois facility. TRAC’s procurement of these chassis aligns with its strategic objective of partnering with key manufacturers in North America to build high-quality chassis.

Any opinions in this notebook represent the author’s views, not the Journal of Commerce, IHS Markit, or S&P Global.

Any rumors in this notebook are just that: rumors. Unconfirmed. Not news stories.

Do you have an opinion or a subject you’d like me to cover? Email me ari.ashe@ihsmarkit.com to send your thoughts.

You may also request the data behind JOC’s Intermodal Savings Index and JOC’s Shipper Truckload Spot Rate Index, available to paid JOC subscribers. Not a paid subscriber? You can change that!

I’d like to remind folks that Norfolk Southern or the South Carolina Ports Authority should not be chided for being transparent, in my opinion. If I had a choice between an entity talking about their successes and failures, or an entity that promotes successes but is absent when there are failures, I’d prefer the former every time. So I respect Norfolk Southern and SC Ports for answering the tough questions when others would go quiet.

We thank our data partners for JOC’s Intermodal Savings Index and JOC’s Shipper Truckload Spot Rate Index: Cargo Chief, DAT Solutions, InTek Freight and Logistics, Intermodal Association of North America, Loadsmart, Sunset Transportation, Transfix, Zipline Logistics, and a JOC survey of 3PLs and shippers.