Festina Lente

Reporter's Notebook: Jan. 27, 2022

Welcome to Edition 13 of the Please Haul My Freight newsletter. Here are some of the items in my notebook this week:

COVID TESTS: Where is your US government supplied COVID-19 test coming from? As Steve Ferreira of Ocean Audit wrote:

“Turn[ing] the back of the box over, you can see it’s made by iHealth Labs, a unit of the Chinese company Andon Health Co., Ltd. They just signed a deal with the US Government for a $1.275 billion contract to provide these tests. Most of these are coming in on Matson, one can only imagine the ocean freight rate for this project.”

Specifically Hong Kong, a special administrative region of the People's Republic of China, according to PIERS, a sister product of JOC.com within IHS Markit.

Not Made in the USA.

Other contracts are with Abbott Labs and Roche Diagnostics Corp, as Ferreira noted.

S.E. PORTS: As the situation gets worse in Charleston, the situation gets better in Savannah. The short-term strategy for Charleston is to barge long-dwelling containers to the Hugh K. Leatherman Terminal and North Charleston Terminal to free up space in the Wando Welch Terminal. Drayage demand is through the roof in Charleston, according to Jason Hilsenbeck of Loadmatch.com and Drayage.com:

“Highest drayage demand in the country, more difficult there now than LA/LB. One importer called [Tuesday] and paid $6,000 to get an import delivered to Alabama. Goes to prove again as any terminal complex gets behind on truck outgates and limits the empty returns, things get really behind and takes months to get terminal back fluid.”

Norfolk Southern has shut down intermodal traffic from Memphis to Charleston, but so far CSX is taking cargo, according to a cotton exporter source.

DEMURRAGE: One perception I may have fostered in previous TPM conferences is that all detention and demurrage is beyond the control of BCOs. That’s inaccurate.

Some of the 4,300 containers dwelling 21+ days in Savannah last September, and 7,000 containers currently dwelling 15+ days in Charleston are importers purposely using terminals as mobile warehouses. Here’s what Jim Newsome of the SCPA told me:

“The vast majority of this is not just ‘oops, it’s not my fault.’ It is all a myth that what's happening out there is all these unreasonable things that nobody has control over. That's just a total crock…

I've got 25,000 important mobile warehouses out on that terminal right now and somebody should legitimately pay for that. A lot of people don't like to hear it, but this is not out of their control… it's absolutely ridiculous to think that this is some burgeoning problem that nobody controls.”

Jim’s position might be polarizing, but D&D is complicated. It’s not black and white. Every case is different. I’ll discuss this at the TPM Conference in late February.

WHEN WILL IT END?: IHS Markit released a report with our experts in automotive, agriculture, energy, labor and materials, and containerized shipping: “The Great Supply Chain Disruption: Why it Continues in 2022.”

Matteo Fini of IHS Markit’s automobile division writes:

“The recent experience of input shortages is forcing automakers to go against everything they have done in the past 30 years when it comes to supply chain management.

This means going against the famous ‘Toyota Way’, which was predicated upon lean supply and having as little inventory as possible. Carmakers are now considering taking on inventory for certain parts because, in relative terms, it costs peanuts to have that inventory compared with having a line stoppage, which can cost upwards of $50 million per week to an original equipment manufacturer.”

PIERPASS: A temporary extension of the PierPass program in Los Angeles and Long Beach expires on Jan. 31, as JOC’s Bill Mongelluzzo writes:

“When the temporary extension to the PierPass program expires Jan. 31, the ports will return to the system they had in place since 2018, under which there’s no financial incentive for truckers to visit during night shifts. The public has 45 days to comment on the requested extension before the US Federal Maritime Commission (FMC) can decide to grant or reject it, though the agency could act in 21 days if the ports file a request for expedited action.”

NS SERVICE: Norfolk Southern on Wednesday acknowledged service was below par in 4Q. Incoming CEO Alan Shaw talked about conversations with his operations team about “restoring our service levels to where we all want it.” And COO Cindy Sanborn said it won’t happen overnight:

“I think we'll be challenged in the first quarter. I think we'll start to see some improvement in the second. As our new employees come on board, I think we'll be back to planned levels of what velocity we have in our plan and what dwell we have in our plan. And that should look closer to what you described as pre-pandemic levels.”

Ed Elkins, chief marketing officer, spoke to intermodal:

“Demand for our intermodal markets is expected to remain favorable, despite continued headwinds associated with supply chain congestion, impacting our ability to capture new opportunities. These headwinds are expected to ease in the second half of the year.”

INLAND POINT INTERMODAL: International intermodal, also known as IPI, plummeted 16.2% in 4Q YoY, reversing a very strong first nine months. IPI plunged 31.2% out of the Southwest, 27.9% out of the Pacific Northwest, and 30.1% out of the Southcentral US (the backhaul lane).

One beneficiary of the IPI decline is the marine chassis providers. Chassis are more available today in Chicago, Memphis, Kansas City, and the Ohio Valley than six months ago. However, TRAC Intermodal and Union Pacific Railroad say IPI volume is picking up in January, so we will monitor this…

TRUCKLOAD RATES: DAT’s wholesale spot rates are up 13 cents to $3.13 through Jan. 24, but there are some early signs of a cooldown in TL rates, writes DAT:

“Seasonality returned to the spot market last week after surprising increases in the prior week. While higher fuel costs lead to increased all-in rates, the line haul portion for dry vans dropped 2 cents per mile…

Load volume in the Los Angeles market increased about 2% last week but outbound volumes have been dropping throughout January (down 40% in the last three weeks)…

Loads from Los Angeles to Chicago are running 30 cents lower than the December average.”

My data pulls on pricing portals show L.A. outbound rates are definitely down sequentially. JOC’s Shipper Truckload Spot Rate Index shows California outbound rates are down 30 cents month over month. Here is more TL data from our partner Cargo Chief1 on the top 200 lanes we track:

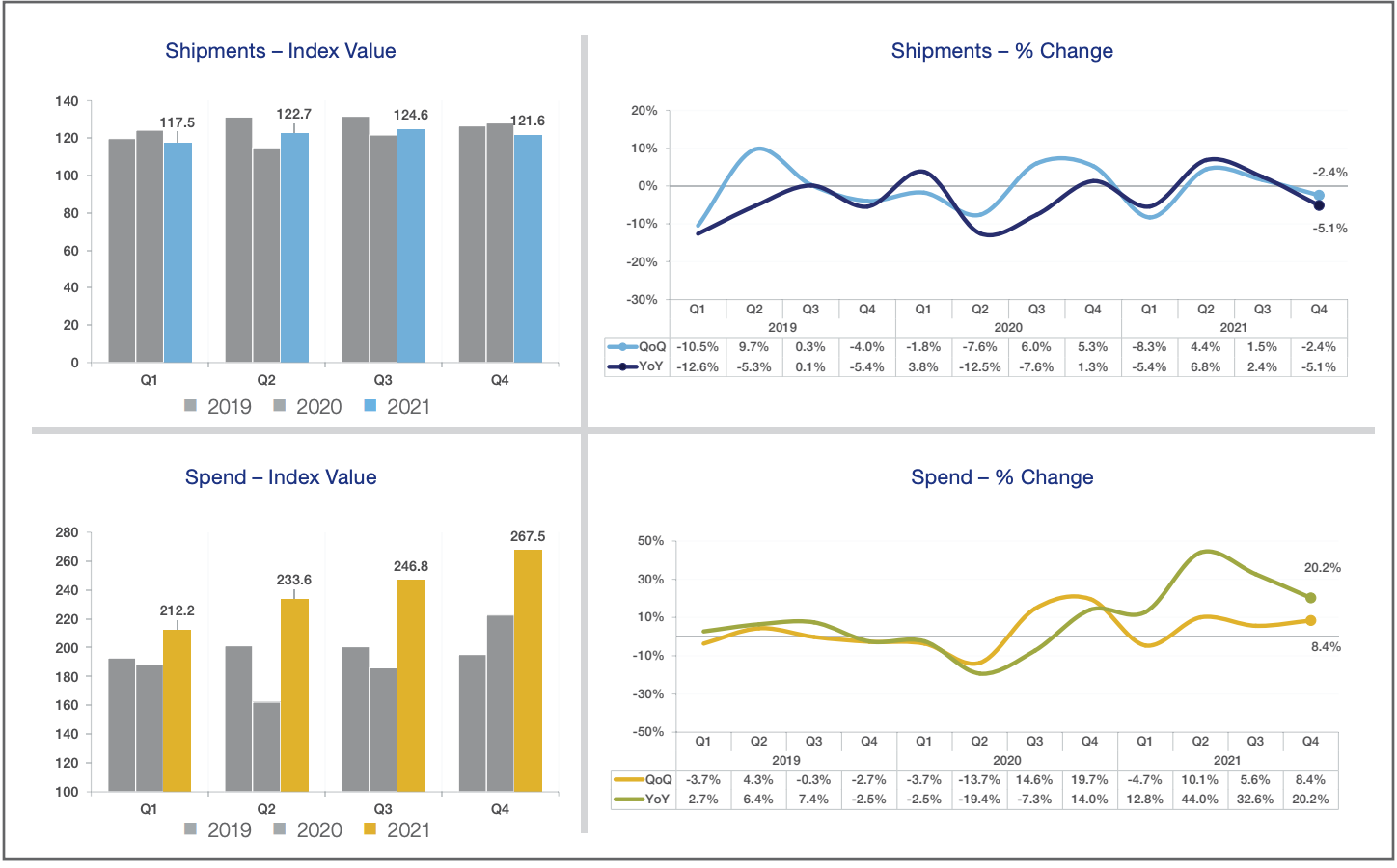

Meanwhile, the U.S. Bank Freight Payment Index was released its 4Q truckload data, which focuses on contract TL freight:

“The U.S. Bank National Spend Index increased, while the U.S. Bank National Shipments Index contracted. Supply chain factors drove softer shipment volumes in Q4 2021. The lack of drivers dedicated to a single company, and a shortage of new trucks and trailers, made it more difficult for fleets to haul more freight, creating more opportunities in the spot market.”

NO PARKING: Bloomberg has a good article entitled “Sleepy Truckers Get Forgotten in Supply Crisis Choking Economy.”

The word “parking” doesn’t appear anywhere in the Biden administration’s 2,333-word “Trucking Action Plan” released last month as part of the rollout of the new infrastructure law during the height of the pre-holiday emphasis on supply-chain snags…

The Federal Highway Administration says the biggest need is within 20 miles of urban areas…

A pilot program in Midwestern states tries to solve the problem with technology: Real-time highway signs showing the number of spaces available at upcoming truck stops, with the data also fed to smartphone apps.

LTL RATES: Saia will implement a general rate increase of 7.5% on LTL and truckload shipments. Here is analysis of Amit Mehotra of Deutsche Bank:

“This appears to be the biggest GRI in at least 10 years for the company, and 200 basis points higher than the GRI this time last year. It also compares to Old Dominion’s +4.9% GRI announced in mid-December…

The key factor that influences the decision-making process of customers when arranging shipments with LTL carriers is service, with price a distant #8; specifically, the top five most critical factors include: (1) shipments delivered with no damages; (2) shipments delivered with no shortages; (3) shipments picked up when promised; (4) billing accuracy, and (5) carrier trustworthiness.”

INTERMODAL CONTRACTS: Union Pacific Railroad is going big on intermodal contracts. One IMC told me that UP’s contract quotes (known as MCPs) on two lanes out of Northern California were +12% to +16% year over year. This is consistent with what UP’s Kenny Rocker said Jan. 20:

“We're about 10% to 15% in on a lot of the bids that we're looking at...Right now it looks good, but we're going to be looking at it quarter by quarter. Great environment to be repricing [for us].”

Non-asset IMCs already tell me UP is also leery about accepting new business in Los Angeles in 2022. UP can be very choosy with what freight to accept with APL, Schneider, and Swift joining the network in 2022-2023.

JOC’s Contract Intermodal Savings Index is at record highs, so the UP can push 12%+ in California and still save shippers money over longhaul trucking. JOC’s Intermodal Savings Index Q4 report will be out next week. The report and data are available to paid JOC subscribers upon request.

HUB GROUP: Dave Yeager will have to answer questions about whether he is fully committed to Union Pacific long term. One industry veteran believes the UP-Hub contract expires December 2023:

“BNSF needs customers other than J.B. Hunt and everyone involved knows it. BN will pursue Hub and make a big run to get them over there. I just don’t think BN can offer them enough to make the change. Hub won’t like being second fiddle to J.B. Hunt. That’s the biggest issue to overcome and the egos involved may make that impossible.”

Schneider may not have liked being second fiddle to J.B. Hunt either. We will never truly know, of course.

AMAZON: Amazon is second fiddle to no one. And one way for BNSF to replace the lost volume of APL, Schneider, and Swift is through Amazon. The e-commerce giant has essentially DOUBLED its 53-foot container fleet in the last six months, according to PIERS data — importing roughly 2,000 containers since August 2021:

NO STRIKE: A federal judge issued a restraining order on Tuesday preventing the union from striking over a BNSF’s new attendance policy starting Feb. 1. The restraining order expires Feb. 8.

UP TRANSLOADS: Union Pacific subsidiary Loup Logistics acquired Precision Components Inc., which has 125,000 square-feet of covered storage and three miles of rail capacity in Phoenix. The facility does not handle containerized goods, but rather forest products, industrial products, bulk commodities, and steel.

PORT OF BALTIMORE: While the Port of Virginia’s funding from the U.S. Army Corp of Engineers got the headlines, the Port of Baltimore received $32.5 million to construct new sites to house dredge material from the Chesapeake Bay.

William Doyle, executive of the Maryland Port Administration, also gave an update Jan. 26 on four ship-to-shore cranes received last September:

“Ports America Chesapeake is load testing those cranes, and the ILA crane operators are up there in the cranes. Each individual crane will be load tested, each individual crane will have training for our longshoreman, and then they will become operational, which will open up the port to more containerized business.”

Laden imports in Baltimore declined 8.9% in 2021, according to PIERS, although two new weekly services into Baltimore may increase volume in 2022.

CHASSIS POOLS: A few chassis items are on my radar screen right now.

DCLI is making headway in putting radial tires on all chassis in Memphis and the Gulf Coast by the end of 2022: 86% in the Gulf, and 80% in Memphis.

The Port of Charleston received the first 700 chassis from THACO Special Vehicle, a Vietnamese-based manufacturer for Pitts Enterprises subsidiary Dorsey Intermodal. The pool of 12,900 chassis will launch in 2023.

TRAC Intermodal said new chassis production is still slow. The US manufacturers have ramped up production, but the latest Omicron surge has introduced new challenges to procure raw materials and subcomponents.

REMINDER: I will moderate a chassis session and an intermodal session at TPM 2022 where we everything in this newsletter and more.

Any opinions in this notebook represent the author’s views, not the Journal of Commerce or IHS Markit. Any rumors in this notebook are just that: rumors. Unconfirmed. Not news stories.

Do you have an opinion on anything I wrote or a subject you’d like me to cover?

Email me ari.ashe@ihsmarkit.com to send your thoughts. You may also request our data behind JOC’s Intermodal Savings Index and JOC’s Shipper Truckload Spot Rate Index, available to paid JOC subscribers. Don’t have a JOC subscription? You can change that!

Cargo Chief, DAT Freight and Analytics, and Loadsmart are three of JOC’s data partners capturing trucking data for our JOC Intermodal Savings Index.