Diving Deep Into J.B. Hunt 3Q2022

Reporter's Notebook: October 20, 2022

Welcome Please Haul My Freight: Edition 31. In this edition we will dive deep into an important theme in my J.B. Hunt’s earnings story.

BOX TURNS: Ok first off, what is a box turn? And how is it measured? Box turns refer to the number of revenue paying loads an average container handles in a month.

Higher box turn ratios mean the supply chain is fluid and drivers and containers are moving with minimal disruptions. That’s good for intermodal providers, for railroads, and for shippers. High fluidity is a win-win.

Slower box turns mean there is disruption in the supply chain. If box turns are down 5% year over year, for example, then an intermodal provider must use more containers, and more drivers to cover the same volume as the prior period.

The intermodal provider spends more in costs, intermodal shippers will see rate hikes.

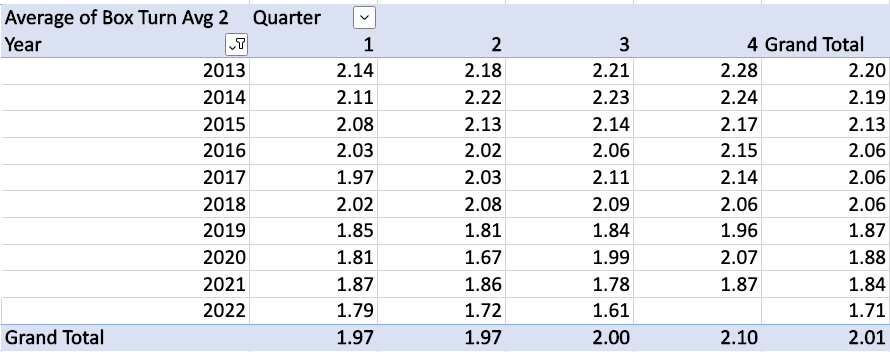

BAD NEWS: I calculate my own estimate of box turns across all US intermodal providers. Unfortunately, they are going in the wrong direction:

If you want more details on how I calculate US box turn data, please reach out to me.

JB HUNT NUMBERS: J.B. Hunt reported box turn ratios fell 6.4% year over year, while I had it down 9.4%:

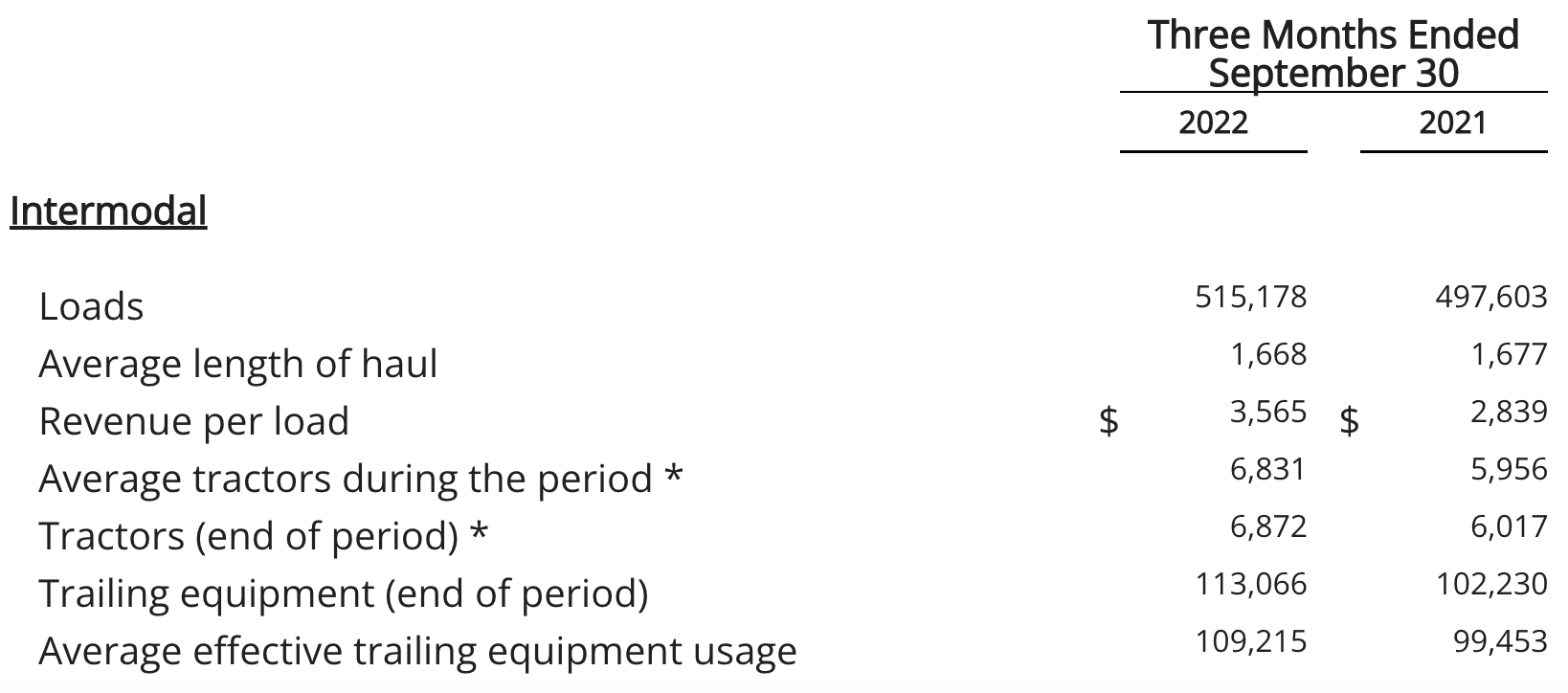

The box turn ratio was 1.52 in the third quarter compared with 1.62 a year ago. If the box turn ratio was flat, instead of down 6.4%, then J.B. Hunt could have handled 550,347 loads last quarter.

In Q3 of 2020, the box turn ratio was 1.81, and if that held to today, then J.B. Hunt would have handled 614,660 loads last quarter!

How did I calculate the box turn ratio? First we divide 515,178 by 113,066, getting us 4.5564 box turns per quarter. Then we divide by three to get 1.5188 box turns per month.

WHAT INFLUENCES BOX TURNS: To understand why box turns rise or fall, we need to walk through what has to occur in sync:

Trains arrive on schedule and containers are made available at a predictable date and time.

The IMC can reliably book a driver to get the container at a specific date and time.

The IMC can reliably book an appointment to deliver the container to the receiver based on #1 and #2.

The receiver quickly unloads the cargo with the necessary labor and warehouse space and returns the empty for the next shipper.

If any of these four falter, then the supply chain slows down and box turns drop.

Larry Gross of Gross Transportation Consulting, one of the smartest intermodal minds (along with Ted Prince), calls this the “intricate, choreographed dance” of intermodal. I can only dream to know 25% of what these men know about intermodal.

WHERE IT WENT WRONG: It has gone wrong everywhere this year. Rail service has been subpar, so #1, #2, and #3 have been largely impossible, but #4 has also gone awry.

However, as we highlighted in “Mr. October” this week, the BNSF on-time performance has improved quite a bit.

Between Sept. 4 and Oct. 7, BNSF’s on-time performance (see below) was 76.6% compared with 59.7% in the final five weeks of the second quarter.

If BNSF or UP can get that number to 85%, then #1, #2, #3 are possible. Now the issue becomes #4.

If inventory levels are high, do receivers have warehouse space to unload containers quickly? Or do they hold onto containers and incur detention? Can companies get rid of inventory to create room in their distribution centers?

And will customers interested in buying items if the discount is big enough?

Those are the questions to monitor in Q4.

WHY DOES IT MATTER: Back to the beginning: if an average container can handle more loads per quarter because #1, #2, #3, and #4 are in sync, then an IMCs costs fall.

If their costs go down, shippers may see those cost savings too. I write “may” because there are other factors such as driver wages, maintenance and repair costs, insurance premiums, among many others.

Will it happen in with 2023 intermodal contracts? J.B. Hunt doesn’t know. I don’t know.

But with truckload contracts that will likely be down year over year in 2023, and continued softness in the truckload spot market, there will be pressure on US railroads and IMCs to hold the line on rates, or seek a very small increase.

INTERMODAL COSTS: Two final thoughts on costs:

If the rail unions approve their contracts in November, then railroads will have additional costs in the new contracts to cover. How that impacts the intermodal rates in 2023 charged to shippers is worth watching.

J.B. Hunt has been using chartered vessels to move containers into the US this year. According to PIERS, a sister product of JOC within S&P Global, roughly 92.2% of all J.B. Hunt’s container came on COSCO and Maersk vessels in 2017. This year, 92.8% of the containers are moving through chartered vessels through China Navigation Co. and Swire Bulk Ltd. (breakbulk), and only 1.8% through COSCO or Maersk. What are the costs to bring containers on chartered vessels compared with Maersk and COSCO? If they are higher on chartered vessels, are the costs passed onto shippers?

Any opinions in this blog represent the author’s views, not the Journal of Commerce, IHS Markit, or S&P Global. Any rumors in this notebook are just that: rumors. Unconfirmed. Not news stories.

Do you have an opinion or a subject you’d like me to cover? Email me ari.ashe@spglobal.com to send your thoughts.

You may also request the data behind JOC’s Intermodal Savings Index and JOC’s Shipper Truckload Spot Rate Index, available to JOC subscribers with the proper subscription tier.

Not a JOC subscriber? Click here to become one.