Freight Report: Rock Bottom, Rock Bottom

Welcome Please Haul My Freight: Edition 32. Here are some items in my notebook this week:

SPOT TRUCKLOAD: After writing there were early signals that the spot market may have bottomed out, rates have reversed course. I must have jinxed it!

C.H. Robinson doesn’t think the bottom will hit until next spring.

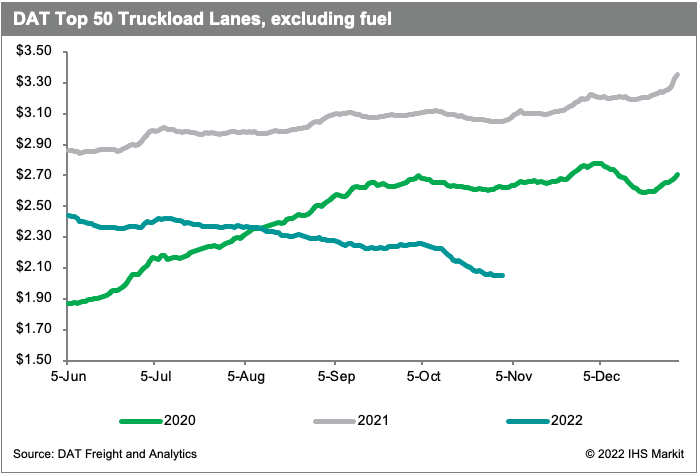

Rates fell $0.12 between Oct. 12 and Oct. 31, according to the DAT Daily Top 50.

The JOC Shipper Truckload Spot Rate Index was up $0.02 per mile early in October but ended the month down about $0.01.

Here is the DAT Daily Top 50, which shows no signals of a peak season.

Tender acceptance rates are also north of 95%, so shippers are not kicking loads rejected by their contract carriers to the spot market.

TRUCKLOAD CONTRACTS: In speaking with a number of shippers over the last few weeks, it’s clear that truckload contract rates will fall in 2023. DAT reports incumbent renewal rates are 8% to 15% lower than prior contracts.

This is consistent with the shippers are telling me:

“We rebid everything over the last month and a half. We had some solid double digit savings across the board, probably 10% to 12% savings. I think we bid it at the right time. That's probably what people are going to see — down 8% to 12% would be my guess.

We didn’t getting much pushback from our carriers. They see what’s happening with the economy.”

Here is what another shipper said:

“It's mostly down high single digits to low double digits. Our carriers have been kicking and screaming too, but I’ve just had heart-to-heart conversations, not only with our carriers, talking to all our vendors about the economy pushing volume down. Some pushback and tell us ‘no’, and then finally give in with some rate reductions.”

JOC INTERMODAL SAVINGS INDEX: We released our JOC Intermodal Savings Index Q3 report on Oct. 31. Our proprietary data shows the average intermodal shipper saved 12.3% on the spot market and 30.3% under an intermodal contract compared with long-haul trucking.

If we assume 95 out of 100 loads move under contract, then our data shows the average shipper saved 27.3% between January 2018 and September 2022, and 26.3% between January 2015 and September 2022.

For October, intermodal shippers saved about 14% on spot market business and 29.5% under contracts, according to preliminary estimates for the JOC Intermodal Savings Index.

INTERMODAL CONTRACTS: It was very telling to me that Hub Group and Schneider National said it was “too early” to discuss intermodal contracts in 2023, as I wrote about in this story.

Here is what Hub Group said Oct. 28, 2021:

“As we look ahead on intermodal pricing, we are feeling very good about the early stages of bid season… Early bid season indications are very strong in continuation of the current trend. We are anticipating a strong bid season.”

Here is what Hub Group said Oct. 27, 2022:

“It's a little early to tell exactly how good season's going to play out, but I think historically intermodal has not moved quite as significantly vertically as truckload. Our focus is going to be really on maximizing our margin per load day. That's how we generate the highest return within the Intermodal segment, and that's going to continue to be the focus for us.”

Schneider’s CEO Mark Rourke similarly talked up rising intermodal contract rates in October 2021, but said it was too early to tell in October 2022. Their silence tells me that pricing power has tipped toward shippers.

Here is what one shipper said:

“If I award the lanes to truckload carriers, I've got a feeling my intermodal partners are gonna come back to me come January, or come after the bid closes and go, ‘Hey, what can you do for me? I can do this now.’ There already was a two-month lag between where the spot truckload rates went and the railroads dropping their rates.”

A second large intermodal shipper agreed:

“There going to have to drop rates. Trucking rates are coming down. They have to see the writing on the wall.”

But what happens if they don’t? Watch local eastern and local western US routes. I see possible conversion on lanes such as Los Angeles to Seattle and Atlanta to Elizabeth, NJ (Croxton-Kearny-Linden). Transcontinental routes (“transcon”) greater than 2,000 miles should stay pro-intermodal because the gap between rail and truck is pretty wide.

THE PUMP: There was a good article in Barron’s about how diesel prices have climbed in recent weeks:

Gasoline prices have started to hit the brakes, but it has been full steam ahead for diesel, with U.S. supplies of the fuel used in freight transportation and agriculture dropping to their lowest on record for this time of year.

That has kept U.S. diesel prices high at the pump, with a gain of more than 8% in October, even as gasoline saw little change to prices this past month, based on data from GasBuddy.

Shortages of diesel fuel around the globe and in the U.S. spurred the latest price advance, says Brian Milne, product manager, editor, and analyst at DTN. Milne refers to U.S. diesel fuel inventory as “extraordinarily low,” with supplies in the Northeast “critically low.”

BNSF: Tom Williams, the head of intermodal for BNSF Railway, released his quarterly video updating intermodal customers on the progress of the network. I spoke with Tom and here were some key highlights:

There are now about 700 ocean containers stacked in BNSF Alliance. If the current trends hold, then the backlog should be cleared within a few weeks. (Note: Sources tell me congestion is a bigger problem in UP’s Dallas terminal.)

The new 1,100 spaces opened recently in BNSF Alliance now creates 8,300 spots for containers, and provides space to flex to ground stack if necessary again.

Congestion is still a problem at BNSF Logistics Park Chicago, Lot 16, Lot 17, as the chassis shortage persists. Turn times averaged 82 minutes in LPC in October.

BNSF has not moved new containers to the ITS Conglobal Joliet facility in five weeks, however, and the stack is down to less than 300 boxes. ITS is more fluid than three months ago.

BNSF chose to use ITS Joliet because the alternative was to keep containers sitting in the Los Angeles and Long Beach terminals. (Some UP-bound boxes have been stuck in the ports for 80+ or 90+ days.)

BNSF is diving deep into technology with J.B. Hunt “on process and technology integration, which drives hub fluidity, even without terminal expansion.” Williams feels the next step is “to better integrate with a more disparate group of drayage carriers, the chassis pool providers, the marine terminals, to use technology to take some of the variability away from all of those different stakeholders that are supporting the IPI supply chain. That's going to be a big opportunity in the future.”

Tom Williams is a great person to chat with and one of the most accessible and brightest intermodal minds in the industry.

UP: Union Pacific CEO Lance Fritz is out with an article defending the benefits of precision scheduled railroading.

PSR consolidates networks, eliminates less efficient moves and increases train size. Fewer trains now move across our system, and at a faster pace. Longer trains deliver significant benefits to customers and remove big trucks from highways. That, in turn, cuts harmful emissions, eases traffic and helps prevent wear and tear on taxpayer-funded roads.

Reducing train size, and therefore increasing the number of trains operating would only exacerbate network congestion and labor challenges.

Give it a read, and tell me what you think.

RAIL LABOR: There are growing concerns about a rail strike right before Thanksgiving. Yes, the strike was averted in September, but a tentative deal is not signed and sealed without the rank-and-file ratification.

We will learn the final vote from the Brotherhood of Locomotive Engineers and Trainmen (BLET) and Sheet Metal Workers Air, Rail, and Transportation (SMART-TD) on Nov. 21. Mark your calendars: that’s a huge day.

The Brotherhood of Maintenance of Way Employees (BMWED) and Brotherhood of Railroad Signalmen rejected their tentative agreements. Seven unions have ratified.

The core issue for the rank-and-file is short-term unpaid sick days. More in the New York Times.

OAKLAND: There was a work stoppage earlier this week at the Port of Oakland. Why does it matter? Minimally, there is an optics problem the West Coast ports must address to restore the confidence of BCOs shifting freight to East Coast ports.

MEXICO: Kansas City Southern Railway broke ground on a second bridge US-Mexico bridge over Laredo. Railway Age has an article on why this will benefit rail customers. The bridge is expected to be complete in late 2024.

GOING UP: TRAC Intermodal will raise rates on Dec. 1, 2022 for chassis, according to a letter sent to customers.

The (rate increase) will enable TRAC to continue our fleet modernization program in our never-ending effort to provide our customers with the industry's safest and most reliable chassis….

Additionally, in order to meet the unprecedented container volume and demand pressure, TRAC increased investment in our overall fleet expansion and modernization during 2022 by more than 60% over the prior year.

CPG: Drayage provider ContainerPort Group is launching an expedited drayage service. More from a press release:

The Expedited Services team will focus on finding solutions to move customer-critical containers that are not easily accessible or otherwise detained at rail yards and container yards across the country…

Many providers are struggling with a lack of equipment needed to get containers moved from storage areas, or a lack of available space at the destination facility. Customers needing immediate assistance can leverage CPG Logistics’ broad network of carrier partners to free their freight from whatever circumstance, no matter the location.

DECK THE HALLS: The National Retail Federation forecasts retail sales will grow 6% to 8% year over year in November and December to $942.6 billion to $960.4 billion. More from NRF President and CEO Matthew Shay on a call with reporters:

“We do know that consumers are looking for discounts. They're looking for deals for value. stretch their dollars in the face of higher energy prices, housing prices. So we know that they're looking for those opportunities. We think that that's going to continue in for the holiday season; they're going to be looking for bargains and values as the holiday season begins in earnest.”

NRF Chief Economist Jack Kleinhenz on the same call:

“We feel very positive that consumer fundamentals will continue to support economic activity, despite the record levels of inflation and rising interest rates.

When we got the third quarter GDP numbers from the Bureau of Economic Analysis, GDP rose by 2.6% and that was more than expected. It was the first increase after two consecutive quarter contractions. This should override any concern at this time that the economy is in a recession. We expect the economy to continue to grow through the remainder of 2022, but at a slower pace than what we saw in the third quarter.”

Any opinions in this blog represent the author’s views, not the Journal of Commerce, IHS Markit, or S&P Global. Any rumors in this notebook are just that: rumors. Unconfirmed. Not news stories.

Do you have an opinion or a subject you’d like me to cover? Email me ari.ashe@spglobal.com to send your thoughts.

You may also request the data behind JOC’s Intermodal Savings Index and JOC’s Shipper Truckload Spot Rate Index, available to JOC subscribers with the proper subscription tier.

Not a JOC subscriber? Click here to become one.